Portfolio Diversification with Precious Metals for People 50+

Many people in their fifties take time to review their overall savings and financial arrangements as they think about the years ahead. The financial landscape has evolved considerably over the past two decades, with periods of notable inflation and market movements that have influenced various assets differently. What was standard practice for previous generations may prompt fresh consideration today.

For those over fifty, personal time horizons frequently extend another twenty to thirty years or longer, depending on individual health and circumstances. Some maintain certain exposures, while others adjust their holdings toward options perceived as more stable. Precious metals, including gold and silver, have formed part of savings and wealth preservation approaches for thousands of years across civilizations.

This article provides general educational information about ‘how to diversify your portfolio with precious metals’ – their historical characteristics, different types, forms of ownership, and common practical considerations. It is not intended as personalized guidance.

Affiliate Disclaimer: This post may contain affiliate links, meaning we may earn a commission if you make a purchase through them — at no extra cost to you. We only recommend products or services we believe may add value to our readers.

We are not financial advisors, nor are we tax or legal advisors. We strongly recommend that you consult with your personal financial advisor, tax professional, and legal counsel prior to making any decisions regarding your savings or retirement accounts.

Historical Context and Characteristics of Precious Metals

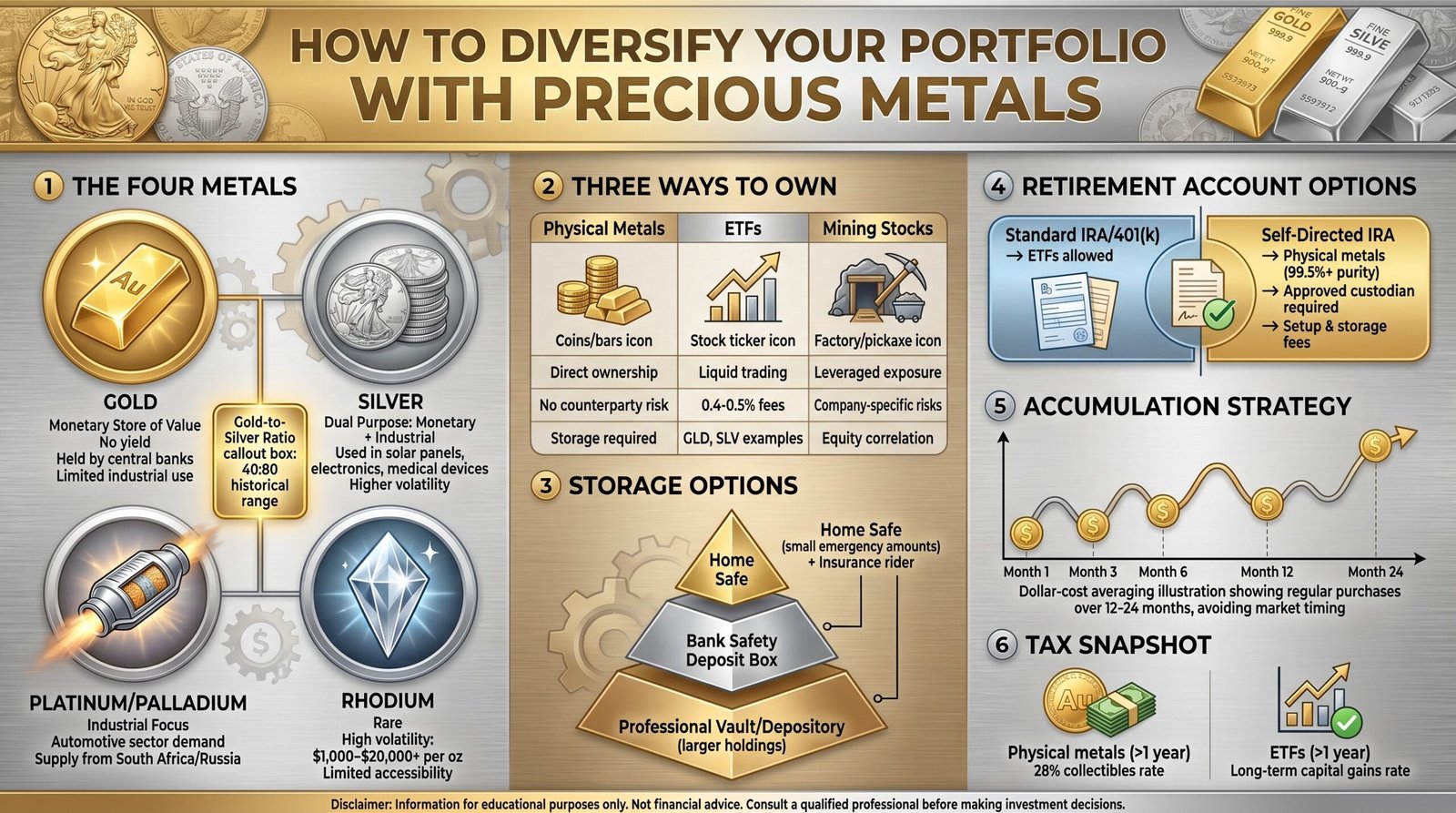

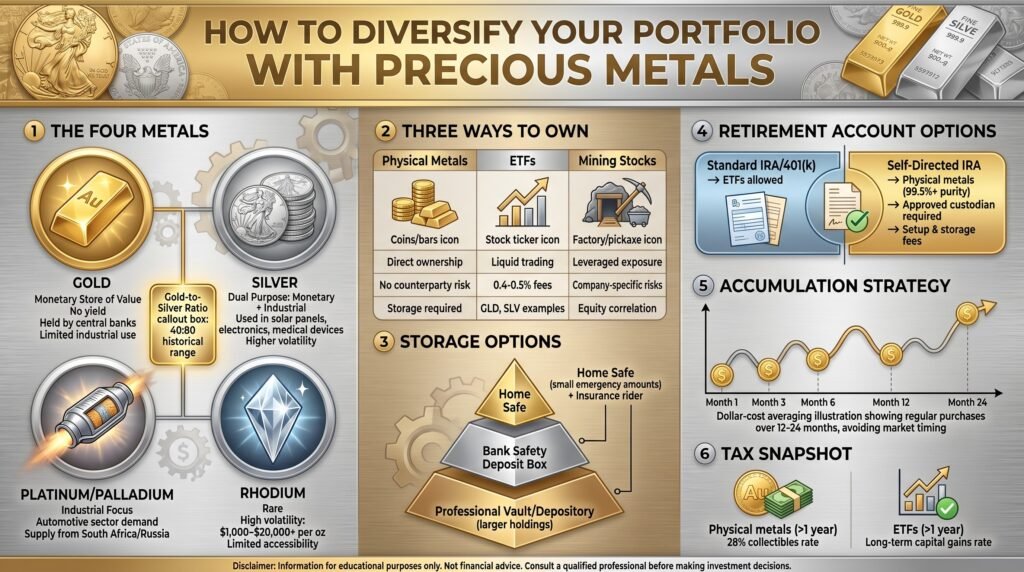

Precious metals have been valued by societies worldwide for millennia. Gold, in particular, has served as a monetary metal held by central banks and individuals during various periods of economic or geopolitical uncertainty. It produces no income or yield and has relatively limited industrial applications compared to other commodities. Its value has historically been tied to collective recognition of its role as a store of value that has endured across cultures and eras.

Silver occupies a distinctive position with both monetary and industrial attributes. It is used extensively in manufacturing, including solar panels, electronics, medical devices, and various industrial processes. This combination of uses can contribute to price movements that differ from those of gold at times.

The gold-to-silver ratio – the number of ounces of silver required to purchase one ounce of gold — has varied over history, often fluctuating within broad historical ranges such as roughly 40 to 80. These past observations are provided for informational purposes only and do not predict future relationships or outcomes. Past price movements or ratios are not guarantees of future results. Nobody can accurately predict future prices of gold, silver, or any other asset.

Platinum and palladium function primarily as industrial metals. Their prices have been influenced by demand from the automotive sector (notably catalytic converters), emission regulations, and supply dynamics from major producing regions such as South Africa and Russia. Palladium, for instance, experienced substantial price changes between 2016 and 2020 linked to shifts in vehicle emission standards and fuel preferences.

Rhodium, another member of the platinum group, is rarer and has shown considerable price volatility in recent decades, with swings from under $1,000 per ounce to over $20,000 at peaks, largely driven by its use in catalytic converters. It is not typically a primary focus for most individuals due to accessibility and product limitations, particularly within retirement accounts.

These metals each respond to different combinations of factors, including real interest rates (nominal rates adjusted for inflation), broader economic sentiment, industrial demand, and supply conditions. Real interest rates have historically played a role in gold’s appeal: when real rates are low or negative, the opportunity cost of holding non-yielding assets changes; when real rates are higher, that opportunity cost increases. However, these are general observations drawn from historical data and should not be interpreted as forecasts.

We are not financial advisors. Any decisions about including precious metals in your arrangements should be made only after consultation with qualified professionals who understand your complete financial situation.

Different Forms of Precious Metals Ownership: Physical vs. Paper

Individuals interested in precious metals often consider both physical ownership and other exposure methods. Each approach has distinct features.

Physical Precious Metals

Physical gold, silver, or other metals in the form of coins or bars represent direct ownership. When held in a personal safe or bank safety deposit box, there is no counterparty risk from financial institutions or funds. Ownership is straightforward: the metal is tangible and independent of broader financial systems.

Popular coins for those exploring physical ownership include American Gold Eagles, Canadian Maple Leafs, and Austrian Philharmonics for gold, along with similar options for silver. These coins are widely recognized, which can aid in authentication and liquidity if selling becomes necessary. Bars may offer different premium structures, particularly for larger quantities, but can be more challenging to divide or authenticate in smaller transactions.

Safe home storage typically involves a high-quality safe rated for the weight and value involved, securely bolted to the floor or wall in a discreet location. Many also obtain a valuable articles rider on homeowners insurance because standard policies often limit coverage for precious metals to modest amounts (commonly $1,000–$2,000). Some choose to keep only limited quantities at home for immediate access and store larger amounts in bank safety deposit boxes or professional vaults.

Exchange-Traded Funds (ETFs) and Paper Exposure

Certain ETFs, such as GLD for gold or SLV for silver, hold physical metal in vaults and issue shares representing fractional ownership. These trade on stock exchanges with the liquidity of equities — shares can be bought or sold during market hours. Expense ratios are generally low, often in the 0.4% to 0.5% range annually. However, owners hold shares in the fund rather than the underlying metal itself, introducing counterparty risk to the fund and its custodians.

In extreme scenarios, such as operational or systemic issues with the fund, the outcome differs from holding physical metal directly.

Mining Stocks and Related Vehicles

Mining companies and mining ETFs provide exposure linked to precious metals production. When metal prices move, mining equities can experience amplified effects due to operating leverage (changes in profit margins). However, these investments also carry company-specific risks, including management decisions, operational costs, regulatory issues, and correlation with broader equity markets that can be higher than that of physical metals.

For retirement accounts, standard brokerage IRAs or 401(k)s typically allow metals ETFs. Physical metals generally require a self-directed IRA with an approved custodian and an IRS-compliant storage facility. These specialized accounts involve setup fees, annual custodial fees, and storage costs that can total several hundred dollars per year, depending on the provider and allocation size. The metals must meet specific IRS purity standards (for gold, typically 99.5% or higher).

Many individuals who explore precious metals use a combination of methods. For example, some hold a portion in physical coins outside retirement accounts for direct ownership and the remainder in ETFs within retirement accounts for liquidity and management ease. Mining-related holdings, when included, are often kept to smaller portions due to their distinct risk profile.

Past performance of any of these methods is not indicative of future results.

Practical Considerations for Accumulation and Management

Timing the acquisition of precious metals can be challenging because price drivers often relate to macroeconomic developments that unfold over extended periods. Some people implement a systematic approach, such as spreading purchases over months or years through dollar-cost averaging. This involves regular, fixed-dollar acquisitions rather than attempting to time market movements.

For physical metals, this might mean establishing an ongoing relationship with a reputable dealer — either online platforms that offer scheduled purchase options or local coin shops that serve repeat customers. Transaction premiums (the difference between spot price and purchase price) apply and should be understood in advance.

For ETF positions within retirement accounts, many brokerage platforms support automated investment plans that purchase shares at regular intervals with low or no transaction fees for eligible ETFs.

Rebalancing holdings when allocations shift is another area of consideration. Traditional annual rebalancing involves returning to target weights, which requires selling after periods of strong performance and buying after weakness. Some prefer wider tolerance bands (for instance, only acting when an allocation moves substantially beyond an intended range) to reduce transaction frequency, associated costs, and potential tax events in taxable accounts.

Physical precious metals held in taxable accounts and sold after more than one year are generally taxed as collectibles at a maximum federal rate of 28%, differing from standard long-term capital gains rates that apply to many other assets. Holdings sold within one year are taxed at ordinary income rates. In contrast, growth within retirement accounts (traditional or Roth IRAs) follows the account’s standard tax treatment — deferred until distribution in traditional IRAs or potentially tax-free for qualified Roth distributions. These are factual descriptions only; individual tax situations vary widely, and professional advice is essential.

Storage and security decisions affect overall costs and accessibility. A balanced approach might distribute holdings across home storage for small emergency amounts, bank safety deposit boxes, and approved professional depositories for larger quantities.

Frequently Asked Questions

How much gold or other precious metals might someone around age 60 consider? General resources and historical discussions sometimes reference ranges such as 5% to 10% of investable assets in precious metals, with gold often forming the largest share within that category. However, there is no universal or recommended amount. The appropriate level, if any, depends entirely on an individual’s complete financial picture, other income sources (such as pensions or Social Security), existing holdings, and personal circumstances. Past examples or general ranges are not advice or guarantees. Consult qualified professionals for your situation.

Can physical gold be held in an IRA? Yes, physical gold and certain other precious metals can be held in a self-directed IRA, provided they meet IRS purity and eligibility requirements and are stored with an approved custodian and depository. Individuals cannot store the metals themselves. Setup and ongoing custodial/storage fees apply and should be evaluated carefully. For many, simpler alternatives like gold ETFs within a standard IRA may be more straightforward and cost-effective, though they involve different ownership characteristics.

What is one common way people acquire precious metals in the context of retirement planning? Some combine physical coins or bars held outside retirement accounts with ETFs inside IRAs or 401(k)s. Common bullion coins such as American Gold Eagles or Canadian Maple Leafs are frequently purchased from established dealers. Inside retirement accounts, low-cost ETFs that hold physical metal in vaults are widely available. These are general methods only; suitability varies by individual.

How does silver compare to gold in terms of characteristics? Silver exhibits greater price volatility than gold, partly due to its significant industrial demand alongside monetary aspects. Gold has historically shown lower correlation figures with equities in long-term data. Some individuals include silver as a complement to gold within any metals exposure, potentially in varying proportions. The gold-to-silver ratio serves as one historical reference tool, but past relationships do not predict future ones. Past performance is not a guarantee of future results.

What are the general tax implications when selling physical gold? Physical gold and silver held for more than one year are classified as collectibles for federal tax purposes, with a maximum long-term capital gains rate of 28%. Short-term holdings (one year or less) are taxed at ordinary income rates. Precious metals ETFs or mining stocks held in taxable accounts follow standard capital gains rules, while holdings inside retirement accounts are governed by the IRA’s tax treatment. These rules are complex and subject to change; always consult a qualified tax professional for advice specific to your circumstances. We do not provide tax advice.

Should someone consider gold coins or gold bars? Coins are often chosen for their recognizability, ease of authentication, liquidity, and ability to be sold in smaller increments. Widely accepted examples include American Gold Eagles, Canadian Maple Leafs, and Austrian Philharmonics, which typically trade with competitive premiums over spot price. Bars can sometimes carry lower premiums for larger purchases but may be more difficult to authenticate or partially sell. The choice depends on individual preferences, purchase size, and intended use.

How can physical gold be stored safely at home? Effective home storage generally requires a robust safe rated for both weight and value, firmly anchored to the floor or wall in an inconspicuous location. A dedicated valuable articles insurance rider is advisable, as standard homeowners policies provide limited coverage for precious metals. Many limit home holdings to modest emergency amounts and utilize bank safety deposit boxes or professional storage facilities for the majority. Professional storage offers insured, secure options but involves fees.

Are gold mining stocks or ETFs commonly included in retirement-related discussions? Mining stocks and ETFs can provide leveraged exposure to underlying metal price movements because company profitability is sensitive to price changes. However, they also introduce additional risks from corporate operations, management, and closer ties to equity market behavior. When discussed, they are sometimes limited to smaller portions of any metals-related holdings to maintain focus on physical metals or ETFs for their distinct characteristics. Past performance of mining equities does not guarantee future results.

Additional Considerations for Those in Their 50s and Beyond

As individuals move through their fifties into their sixties and beyond, approaches to any asset class, including precious metals, may evolve. Early in the decade, some maintain broader exposure across metals; later, there may be a gradual shift toward more established options such as gold. Liquidity and ease of management often become higher priorities closer to or during retirement years.

Systematic accumulation over 12 to 24 months or longer can help address the difficulty of timing. Rebalancing with wider bands may reduce unnecessary transactions while allowing positions to respond to market conditions naturally.

Storage strategies frequently emphasize distribution: a small amount in accessible home or bank storage combined with professional depository options for the balance. Costs – including premiums, fees, insurance, and storage – should be understood upfront as they reduce net returns.

Legacy planning in later decades may involve considerations around titling, beneficiary designations, and ease of transfer, particularly within or outside retirement accounts.

Throughout all stages, the core principle remains education and professional consultation. Precious metals have unique attributes compared with other assets, but they also carry risks including price volatility, storage responsibilities, liquidity differences, and costs.

Key Takeaways

- Precious metals encompass gold (primarily monetary), silver (monetary and industrial), and platinum-group metals (largely industrial). Each has responded differently to economic conditions historically.

- Ownership options include physical coins/bars for direct possession, ETFs for liquidity, and mining-related vehicles for leveraged but more equity-correlated exposure.

- A combination of physical holdings outside retirement accounts and ETFs inside them is one approach some individuals use to balance direct ownership with practical management.

- Systematic purchase plans and wider rebalancing bands are methods that help manage implementation without attempting precise market timing.

- Storage and security require careful planning, balancing accessibility, cost, and protection.

- Tax treatment differs by account type and holding period; physical metals in taxable accounts face collectibles rates.

- All decisions must be based on personal circumstances after consulting qualified financial, tax, and legal professionals.

We are not financial advisors. Nothing in this article constitutes investment, financial, or tax advice. Past performance is not a guarantee of future results, and nobody can predict future prices or economic conditions.

If you would like to learn more about precious metals and options available for retirement accounts, I suggest contacting Augusta Precious Metals to request their free Gold IRA guide and educational materials. Their resources provide additional information on IRS-compliant processes and product options.

This review provides detailed information regarding Augusta Precious Metals for your reference.

Leave a Reply