In the realm of precious metals IRAs, Birch Gold Group stands out as a prominent player, with thousands of customers sharing glowing testimonials about their seamless experiences, knowledgeable representatives, and efficient transactions.

Founded in 2003 and headquartered in Burbank, California, the company has built a reputation for helping investors diversify their retirement portfolios with gold, silver, platinum, and palladium. Endorsed by figures like Ben Shapiro and Ron Paul, Birch Gold Group boasts high ratings across platforms: an A+ from the Better Business Bureau (BBB), AAA from the Business Consumer Alliance (BCA), 4.9/5 on Trustpilot, and 4.8/5 on Google Reviews.

Yet, beneath this positive surface lies a more complex story. Industry experts and customer complaints highlight structural challenges that could gradually erode returns, such as high premiums on certain products and fee structures that affect smaller accounts. Understanding both sides is crucial before committing your retirement savings to Birch Gold Group. This Birch Gold Group review draws on recent analyses from 2026 to provide a balanced, fact-based examination.

Affiliate Disclaimer: This post may contain affiliate links, meaning we earn a commission if you purchase through them – at no extra cost to you. We only recommend products or services we believe add value to our readers.

The Commission Model at Birch Gold Group

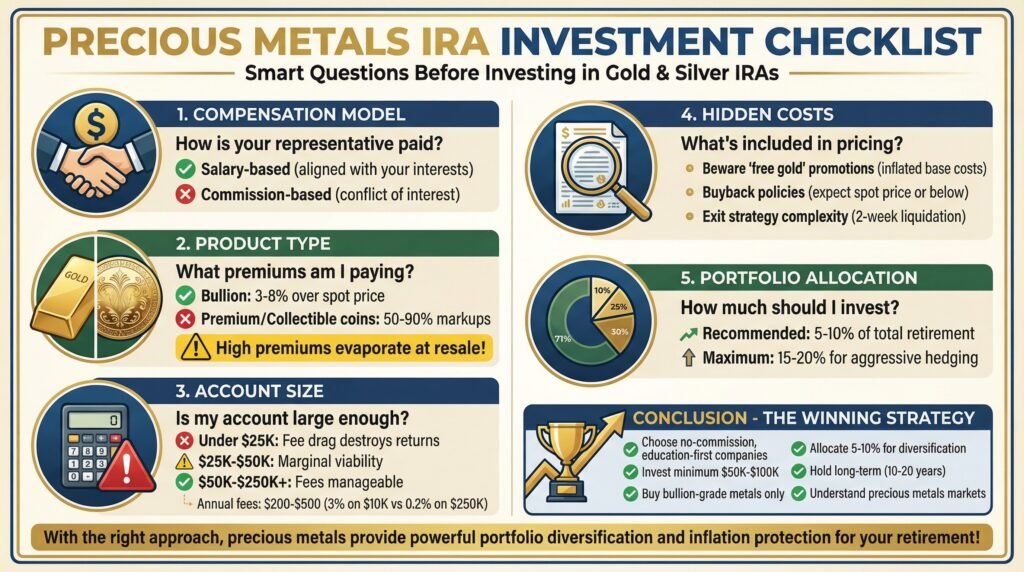

Birch Gold Group operates on a commission-based sales structure, where representatives earn based on the products sold and transaction size. This model, common in the industry, can create inherent conflicts. A sales rep might prioritize higher-margin items like premium coins over lower-margin bullion, even if the latter better aligns with long-term retirement goals. For instance, premiums on commemorative or collectible coins can reach 50-90% over spot price, boosting commissions but potentially eroding investor value.

Customers have reported feeling steered toward these high-premium options during consultations. One 2026 complaint detailed being charged a 73.8% premium on gold and an 81.73% premium on silver, far exceeding industry standards of 10-20%. While reps may believe in the products’ potential, the incentive structure—tied to quotas and revenue—can subconsciously influence recommendations.

Birch Gold emphasizes education, offering free information kits and resources on its website, but the commission structure remains a key concern. Over decades, unnecessary premiums mean less capital compounding for you, turning a protective hedge into a costly one.

Premium Products vs. Bullion Grade Metals with Birch Gold

Premium products dominate the offerings at commission-driven precious metals dealers. These are specially minted coins, commemorative editions, proof sets, and collectible items that sell for substantially more than their metal content alone would justify.

When you buy a standard gold bullion bar at 3-5% over spot price, you’re essentially purchasing the pure metal value with a small transaction cost built in. When you buy a premium coin at 50-90% over spot price, you’re paying for perceived collectibility, rarity, condition grading, and aesthetic appeal. The problem is that most of this premium value only exists in the retail market where you bought it.

When you eventually need to sell, you’re selling back into a wholesale market that primarily values metal content.

Birch Gold Group’s product lineup includes both bullion-grade metals and premium items. Bullion, such as standard bars, rounds, or coins like the American Eagle or Canadian Maple Leaf, trades close to spot price with minimal markups (3-8%). These are valued primarily for their metal content, making them ideal for pure investment plays.

Premium products, such as limited-edition coins like the Britannia series or proof sets, command higher prices due to their rarity, design, and collectibility.

The issue arises at resale. Premium coins often lose their markup in wholesale markets, where buyers focus on melt value. A $50,000 investment in premium coins might yield only $30,000 in actual metal, requiring gold prices to nearly double just to break even. Complaints against Birch Gold echo this: investors report being pushed toward “rare” coins with 50-75% premiums, only to face steep losses upon liquidation.

Bullion, by contrast, captures nearly all of gold’s appreciation from day one.

Birch Gold offers both, but the sales process may emphasize premiums to boost its higher margins.

Investors should insist on bullion if seeking straightforward diversification.

Free Gold Promotions and Inflated Basis Costs

You’ve probably seen the advertisements: “Open a gold IRA and receive $5,000 in free silver!” or “Bonus gold with qualifying rollovers!” These promotions feel like you’re getting something valuable at no cost, but they actually represent one of the most expensive “free” things you can receive.

The “free” precious metals get factored into your overall purchase price through higher premiums on your main purchase. You might pay 60% premiums on your primary gold allocation instead of 40% premiums, with that difference funding your “bonus” metals.

Birch Gold frequently promotes “free” precious metals, such as up to $20,000 in bonus silver or gold on qualifying rollovers of $50,000+. These incentives sound appealing, but often come at a hidden cost. The “free” metals are funded by increasing the premium on your main purchase—say, 60% instead of 40%. This inflates your overall basis, meaning you need greater metal price gains to profit.

Recent reviews warn that these bonuses use lower-value items with inflated retail pricing, worth far less at buyback (e.g., a $5,000 “free” silver bonus might fetch $1,200). Psychologically, it anchors you to Birch Gold, reducing the likelihood of shopping with competitors. While the company positions these as genuine perks, they restructure margins rather than add true value. Always calculate the effective premium post-promotion to assess real costs.

The Minimum Investment Mismatch

Birch Gold’s $10,000 minimum is accessible, but fixed annual fees, around $180-230 (including $80 custodian, $100 storage, and setup), can drag on smaller accounts. For a $10,000 IRA, that’s a 2-3% expense ratio, compared to 0.03-0.20% for traditional funds. Over 20 years, fees could consume $4,000-6,000, requiring metals to appreciate just to break even.

Accounts under $50,000 often underperform due to this drag, yet Birch Gold accepts them for immediate revenue. Larger accounts ($250,000+) absorb costs better.

If your IRA is small, consider whether the structure suits your timeline since long horizons amplify the impact of fees.

Exit Strategy Complexity

One aspect of the sales process that doesn’t get nearly enough attention is what happens when you eventually need to access your money. Selling precious metals isn’t like selling stocks, where you click a button and have cash in your account two days later at precisely the market price.

Premium coins create particularly difficult exits. If you own rare commemoratives or high-grade collectibles, you need to find buyers who value those premium characteristics.

This takes time, specialized knowledge, and often involves consignment arrangements or auction processes.

During this period, gold prices might move against you, eating into your returns.

Even with standard bullion, you’re dealing with bid-ask spreads, dealer buyback policies, and timing considerations. Many companies offer buyback programs, but they’re under no obligation to pay anywhere near retail prices.

You might learn that the company cheerfully sells coins at 50% above spot but only buys them back at 5% below spot, a 55% round-trip cost you’ll only learn when it’s too late to matter.

I think understanding this before you invest matters deeply: precious metals are relatively illiquid assets with meaningful transaction costs on both ends. This doesn’t necessarily make them bad investments, but it does mean they function very differently from the stocks and mutual funds you’re probably used to.

If you don’t understand those differences upfront, you’re likely to experience unpleasant surprises at exactly the wrong moment.

The timing issue becomes particularly acute during market volatility. Let’s say you need to take a required distribution from your IRA, and gold is down 20% from its peak.

With precious metals, you first need to contact your custodian, who contacts their liquidation partner, who makes you an offer that’s probably 5-8% below spot price. By the time the transaction settles, prices might have moved further against you.

The entire process could take two weeks, during which you have zero control over your exposure.

Selling with Birch Gold involves their buyback program, but it’s not as simple as liquidating stocks. Premium coins require finding buyers who value collectibility, often via auctions or consignments, delaying funds and exposing you to price swings. Even bullion faces bid-ask spreads.

Custodians like Equity Trust or STRATA handle sales and partner with depositories (e.g., Delaware Depository, Brink’s). Processes can take weeks, especially during volatility. Required minimum distributions (RMDs) at age 73 mean selling portions annually, taxed as income.

When Precious Metals IRAs with Birch Gold Actually Make Sense

Despite everything I’ve outlined, there are scenarios where precious metals allocations serve legitimate portfolio purposes. The key is matching the product structure to your specific situation and timeframe.

If you have a substantial IRA, say $250,000 or more, and you want to allocate 5-10% to precious metals as a hedge against currency devaluation or systemic financial instability, that allocation can make mathematical sense. The account size absorbs the fixed costs efficiently, and the allocation percentage prevents over-concentration in an asset class with high transaction costs.

If you genuinely understand precious metals markets, actively track spot prices, and can assess whether dealer premiums are reasonable, you’re operating from knowledge rather than sales pressure. You can insist on bullion-grade products, negotiate better pricing, and make informed timing decisions.

If you’re in your early retirement years (55-65) and want a portion of your portfolio in physical assets that aren’t correlated with stocks and bonds, precious metals serve that portfolio construction role reasonably well. You have enough time horizon to weather volatility, but not so much time that fee drag becomes overwhelming.

The people who really shouldn’t be moving retirement money into precious metals IRAs are those with small accounts, long time horizons, limited knowledge of metals markets, and expectations shaped primarily by promotional materials rather than independent research. Unfortunately, this describes a large percentage of the people who actually open these accounts.

Birch Gold shines for mid-to-large accounts ($50,000-$250,000+) seeking 5-10% allocation as a hedge against inflation or instability. If you’re 55-65, knowledgeable about markets, and value education (via their kits, videos, and articles), it’s a fit. Their transparency in flat fees benefits high-balance investors.

Birch Gold Group provides this information to you at NO cost or Obligation to you.

The Education-First Alternative Model

Some precious metals companies have structured themselves differently, eliminating commissions entirely and compensating representatives through salaries rather than sales incentives. This changes everything about how the relationship functions.

When your advisor doesn’t earn more by selling you premium products, they can honestly recommend bullion-grade metals with minimal markups. When they don’t get paid based on your account size, they can candidly tell you if your IRA is too small to make sense in this structure.

When their compensation doesn’t depend on closing your sale this week, they can encourage you to take six months to research and compare alternatives.

These companies typically have higher minimum investments, often $50,000 to $100,000, because they’re filtering for accounts that actually make structural sense. They also tend to emphasize education rather than urgency, providing detailed materials on how precious metals work, realistic return expectations, and how allocation percentages should vary based on your overall portfolio.

The tradeoff is less hand-holding and fewer warm-fuzzy customer service touches. Commission-driven companies excel at making you feel valued and supported because that personal relationship drives sales.

Education-first companies assume you’re a sophisticated investor who values information over emotional reassurance.

Neither model is inherently superior for everyone. If you’re someone who genuinely values guided support and is willing to pay premium pricing for that experience, commission-driven companies deliver real value.

If you’re analytically minded and prioritize cost optimization over service touches, education-first structures are better suited to you.

Birch is commission-driven, excels in service, prompt responses, and ongoing support.

Please ensure that their incentives perfectly align with your long-term outcomes objective.

Frequently Asked Questions About Birch Gold Group

Can I hold physical gold in my IRA with Birch Gold?

Yes, via a self-directed IRA, but metals must remain with an IRS-approved custodian, such as Delaware Depository—you can’t possess them personally.

What’s the difference between numismatic coins and bullion at Birch?

Numismatic (premium) coins value rarity and history, with high markups; bullion focuses on metal content, with low premiums.

How much are Birch Gold’s annual fees?

Typically $180-230 flat, covering custodian ($80-100) and storage ($100-150), and administrative fees.

What happens at age 73?

You must begin taking required minimum distributions, just as with any traditional IRA. Your custodian will sell enough metals to generate cash for your distribution, which gets taxed as ordinary income.

RMDs require selling metals for cash distributions, taxed as income.

Are precious metals IRAs better than regular ones?

They serve different purposes. Precious metals IRAs offer portfolio diversification and inflation protection, but come with higher fees and transaction costs.

Regular IRAs typically provide better long-term returns through equity and bond investments with lower expenses.

Can I buy from any dealer?

No—purchases go through Birch and their custodians.

What’s a reasonable premium?

For bullion products, premiums of 3-8% over spot are reasonable.

Premiums of 20-40% or higher typically show collectible or commemorative products that may not hold their value at resale.

Does Birch buy back metals?

Most companies offer buyback programs, but they’re not required to pay retail prices. Expect buyback offers at or slightly below spot price, regardless of the premium you originally paid.

Is $25,000 enough?

Most $25,000 accounts struggle with fee ratios that consume too much of potential returns. Accounts below $50,000 face significant structural disadvantages unless you pay very low premiums and minimal annual fees.

What portfolio percentage of my retirement should be in precious metals?

Financial advisors generally recommend 5-10% for diversification purposes, with some aggressive allocations reaching 15-20% for those particularly concerned about currency risks.

Key Takeaways

The precious metals IRA industry operates on a commission-driven model in which sales representatives earn money based on transaction volume and margin, not on whether your retirement outcomes are successful decades later. This misalignment creates predictable consequences that disadvantage most retirement investors.

Small accounts below $50,000 struggle to overcome fixed annual fees, resulting in negative risk-adjusted returns even when precious metals perform well. Companies that accept small accounts with low minimums are prioritizing their immediate commission revenue over your long-term suitability.

Customer satisfaction ratings measure service quality, not investment outcomes, which explains why companies can simultaneously maintain excellent reviews and implement structurally problematic business models. Operational excellence doesn’t compensate for incentive misalignment.

Birch Gold Group’s commission model prioritizes sales over long-term suitability, often leading to high-premium coin recommendations that evaporate at resale.

Bullion is superior for investment, but margins are driven by premiums.

Small accounts face fee disadvantages, and promotions mask inflated costs.

Education-first companies with no-commission models eliminate the structural conflict between representative compensation and customer outcomes, typically resulting in better long-term performance despite less emotional hand-holding during the sales process.

Key Questions and Clarifications for Discussions with Birch Gold Group

To optimize your gold and silver investments, prepare these during consultations:

- Product Recommendations: What percentage premium over spot is this coin/bar? Why premium over bullion? Show math on long-term returns assuming 5% annual gold appreciation.

- Fees and Costs: Break down all fees, including hidden ones in promotions. For my account size, what’s the effective annual expense ratio? How does it compare to a traditional IRA?

- Buyback Details: What’s your buyback price for recommended products today? What’s the bid-ask spread? Provide examples of past client liquidations.

- Risks and Suitability: Is my account size/time horizon suitable? What if metals underperform—exit options? Alternatives to premiums?

- Independence: Are reps commissioned? How does that affect advice? Can I get bullion-only quotes?

- Performance Projections: Provide realistic 10-20-year scenarios that factor in premiums, fees, and taxes. What allocation fits my portfolio?

- Complaints Resolution: How do you handle premium evaporation complaints? Examples?

Clarifying these ensures alignment with your goals and minimizes risks for a fruitful outcome.

Birch Gold Group provides you with this FREE information at NO cost or OBLIGATION to YOU!

Leave a Reply